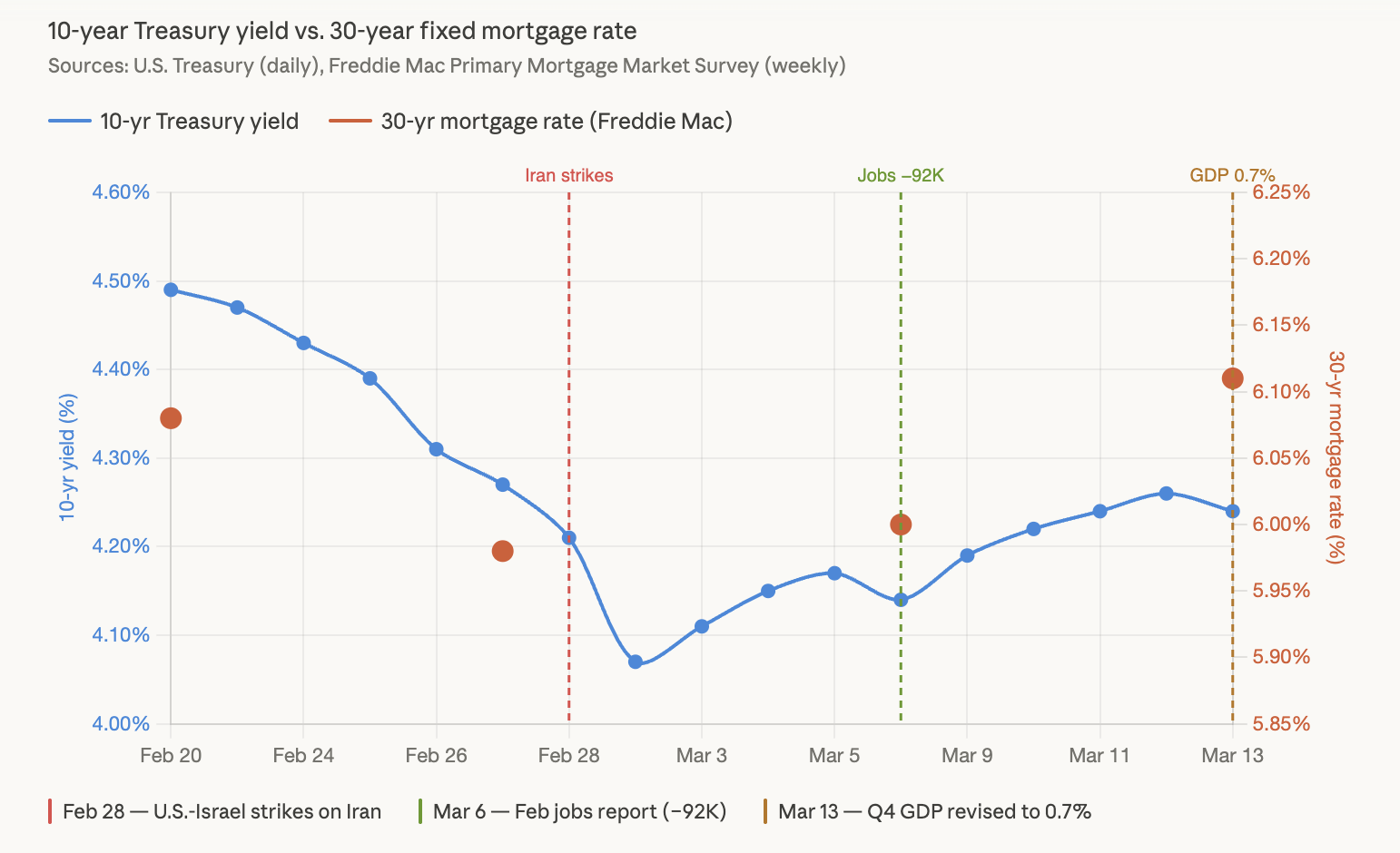

The mortgage market entered March with something it hadn’t seen in years: momentum. Rates had briefly touched 5.98% on February 26, the first sub-6% print since 2022. Purchase applications were running 12% above the prior year. The spring buying season was shaping up to matter. Then the bombs started falling, and the data that was supposed to push rates lower started getting ignored entirely.

The Floor That Held for Two Days

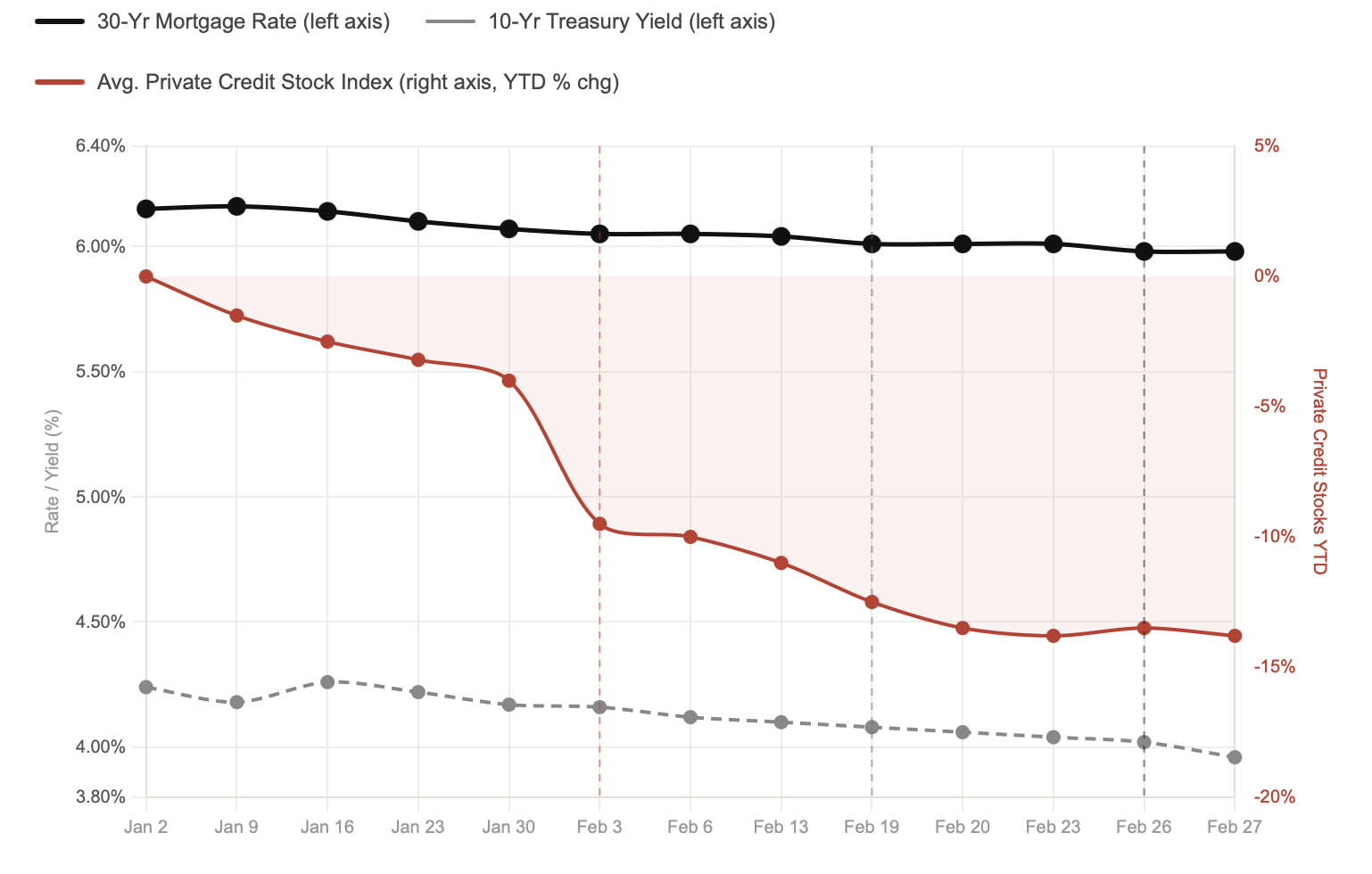

Before the U.S.-Israel strikes on Iran, the rate environment had been quietly improving. The advance Q4 2025 GDP estimate, released February 20, came in at 1.4%, already a steep deceleration from 4.4% in the third quarter, and a number that signaled the economy was cooling faster than the Fed’s December projections had anticipated. The 10-year Treasury had been responding, drifting down toward 3.93% in overnight trading by end of February, its lowest level in nearly a year. At that yield, the math was pointing toward 30-year rates in the high 5s through the spring. The mortgage industry had real reason to believe the floor was giving way downward.

The strikes launched February 28. The initial Treasury reaction was textbook, a brief safe-haven bid pushed yields lower as investors moved into duration on the shock. It didn’t last more than a session. Oil prices started climbing almost immediately on fears of supply disruption through the Strait of Hormuz, and as oil moved, inflation expectations moved with it. The 10-year reversed course and started climbing. By early March it was back above 4.10%, and it kept going.

Then the labor data came out, and the bond market made its priorities clear. On March 6, six days into the war, the February jobs report landed: the economy shed 92,000 positions against an expectation of 70,000 gains, the unemployment rate rose to 4.4%, and private-sector payrolls fell 86,000. Under normal conditions, a print like that would have been a significant Treasury rally event. Yields dipped about 6 basis points in the immediate aftermath. Then oil pushed past $90 a barrel, the move reversed almost entirely within the same session, and the 10-year closed the day nearly flat. On Friday, the second estimate of Q4 2025 GDP was revised down further to 0.7% from the already soft 1.4% advance print, a dramatic deceleration from the 4.4% growth posted in Q3. The 10-year was little changed on the day. The bond market had effectively told us everything we needed to know about what was running the show: two consecutive pieces of data that in any other environment would have driven yields meaningfully lower were smothered by the inflation signal coming from oil.

The Oil Shock and What It Does to the Playbook

The conventional geopolitical transmission works like this: conflict drives safe-haven flows into U.S. Treasuries, yields fall, mortgage rates follow. That is not what happened here, and understanding why is the key to reading where rates go from here.

This war is an inflation event. Iran’s declaration that the Strait of Hormuz would remain closed cut off a waterway carrying roughly 20% of the world’s daily oil and LNG supply. Brent crude has surged more than 36% since the conflict began. WTI is up roughly 39%. Oil is trading above $100 a barrel and Qatar’s energy minister has warned of scenarios that could push it toward $150 if disruptions persist. As a result, Goldman Sachs raised its year-end PCE inflation forecast by 80 basis points to 2.9%.

That kind of supply shock doesn’t drive Treasury yields lower. It drives them higher, because what investors are pricing is not fear, it is the inflation the disruption produces. Higher oil means higher consumer prices, which means fewer Fed cuts, which means long-duration bonds get repriced. The bond market read it that way and moved before most of the sell-side caught up. The same dynamic that in a different conflict might have produced a sharp Treasury rally instead produced the opposite, because this particular shock lands on an inflation picture that was already running above target for a fifth consecutive year heading into the conflict.

The result is a stagflationary setup taking shape in real time. Growth was already slowing, the GDP revision to 0.7% is somewhat of a warning. The labor market is losing jobs. And the inflation that had been trending toward the Fed’s 2% target is now being pulled in the wrong direction by an energy shock that will work its way through gasoline prices, transportation costs, and broader consumer prices in the months ahead, if not contained. Slowing growth and reaccelerating inflation is not a combination the Fed has a clean policy response to, and the mortgage market is sitting directly in the crossfire.

A Double Tax on Spring Buyers

What makes the current rate environment particularly punishing is that borrowers are getting hit on both legs of the mortgage rate calculation simultaneously.

The first leg is the 10-year Treasury yield, which went from 3.93% to above 4.25% in under three weeks, driven by a bond market that is pricing oil-driven inflation and no longer inclined to treat bad labor data or weak GDP as a rate-cut signal.

The second leg is the MBS spread, the additional compensation investors demand to hold mortgage-backed securities over Treasuries. Higher volatility has pushed MBS current coupon spreads back to the widest level since December, more than fully offsetting the spread tightening that had helped bring rates under 6% in January. When spreads widen, mortgage rates move higher even when Treasury yields hold flat. When Treasury yields are simultaneously rising, the two forces compound. Capital markets desks that were repricing rate sheets favorably through January and February are now repricing in the other direction, sometimes multiple times in a single day.

That dynamic is landing at the worst possible moment for the housing market. The spring buying season had been building real momentum on the back of the sub-6% rate environment. Purchase application volumes were running 12% above the prior year as recently as early March. What happens to that momentum if tension continues is the question.

What Wednesday Actually Means

The FOMC meeting on March 17-18 is a foregone conclusion on the headline number. A hold at 3.50% to 3.75% is priced at roughly 98%, and no serious market participant is arguing otherwise. The rate decision is not the story. The story is the dot plot, the updated Summary of Economic Projections, and Powell’s press conference. This is the first meeting where the committee must formally incorporate a war it did not anticipate, an oil shock it cannot control, and an economy that in the past two weeks alone has delivered a pessimistic jobs report and a GDP revision that barely registered in the bond market because oil was louder.

The December dot plot penciled in one 25 basis point cut for 2026. The market is now asking whether that dot holds or migrates toward zero. Goldman Sachs, which had been forecasting cuts in June and September, pushed its first cut call to September and December last week, citing rising inflation risks. J.P. Morgan Research went further, moving to no cuts this year. Futures markets, which were pricing three cuts starting in June as recently as late February, have been stripped down to at best one cut in the back half of the year, with the odds of a September move sitting around 40%.

The question that will determine how the mortgage market trades out of Wednesday is not what the Fed does, it is what the Fed says about the tension it now formally sits inside. There is a credible camp within the FOMC, represented by Governor Waller, that argues the labor market deterioration should eventually open the door to easing regardless of oil-driven headline inflation, that energy shocks are transitory by nature and the jobs picture is the more durable signal. If that view gains traction in Powell’s language Wednesday, rates desks will read it as a dovish lean. If Powell instead emphasizes that headline inflation running above target for a fifth consecutive year constrains the committee’s ability to move, the back end of the curve will reprice accordingly.

Leave a Reply