The Fed’s Bind

At its March 18 meeting, the Federal Open Market Committee voted 11-1 to hold the federal funds rate at 3.5% to 3.75%, the second consecutive hold after three quarter-point cuts to close out 2025. The decision itself was never in question. What mattered was the language around it and what the updated Summary of Economic Projections revealed about where the committee thinks this goes.

The dot plot still shows one cut in 2026 and one in 2027. But the Fed revised its 2026 PCE inflation forecast higher, to 2.7%, and by Wednesday afternoon CME FedWatch was pricing in no cuts at all this year. Those two things can both be true simultaneously: the committee’s median projection can show one cut while market pricing reflects the increasing probability that the bar for that cut is unreachable.

Powell said it plainly at his press conference:

“The rate forecast is conditional on the performance of the economy. So, if we don’t see that progress, then you won’t see the rate cut.”

That is not hedged language. It is a conditional with a clear consequence attached. And the inflation progress Powell needs to see was already proving elusive before a barrel of oil crossed $100. PCE ran at 2.4% in February. The February PPI came in hot. The pre-conflict data had not given the committee clearance to cut. The oil shock didn’t create the problem, it amplified a problem that was already there and extended the timeline for resolving it.

The Chokepoint

The Strait of Hormuz has been a theoretical risk for decades. What is different in March 2026 is that the theoretical became operational. Iran effectively closed the strait to Western commercial shipping beginning March 4, threatening and carrying out attacks on vessels attempting transit. Major carriers suspended operations in the corridor. War-risk insurance premiums made commercial transit economically unviable for most operators even absent the direct threat of attack.

The scale of the disruption warrants context. The 1973 Arab oil embargo removed roughly 4.4 million barrels per day from global supply, about 7% of world consumption at the time, and caused a 300% price increase. The Hormuz closure is disrupting up to 20 million barrels per day, roughly 20% of global supply. Energy analysts have described the current shock as three times the scale of the combined impact of the 1970s embargoes. The buffers are better today, the IEA coordinated a strategic reserve release, Saudi Arabia is diverting some volume through its East-West pipeline, but none of the available workarounds come close to replacing normal Strait volumes. Three weeks in, with Iran’s new supreme leader signaling the closure will continue as a pressure tool, the market is no longer pricing a quick resolution.

Corn and the Strait

The oil price story is the one getting coverage. The fertilizer story is not, and it is the mechanism that turns an energy shock into a multi-quarter food inflation problem.

About one-third of global seaborne fertilizer trade passes through the Strait of Hormuz. Gulf countries are major producers of nitrogen fertilizers, which depend on natural gas to synthesize ammonia. That ammonia is now stranded, and nearly a million metric tons of fertilizer cargo is physically stuck in the Gulf with no viable route out. There is no infrastructure workaround, Saudi Arabia built a pipeline enabling oil exports to bypass Hormuz, but no equivalent exists for ammonia or sulfur.

The timing is particularly bad. Farmers typically order fertilizer in March to apply in April or May. Vessels from the Persian Gulf to the U.S. Gulf Coast take roughly 30 days, meaning supply disrupted now will miss the peak spring planting window entirely. Urea prices surged more than 30% since the war began. USDA projections suggest farmers are already shifting away from fertilizer-intensive crops like corn toward soybeans, a planting decision that shows up in food prices later in the year, when the harvest that wasn’t planted arrives at the grocery store as a shortage.

This is the second-order inflation channel that the Fed cannot model precisely but cannot ignore. Energy prices hit CPI with a lag of weeks. Food prices hit CPI with a lag of months. The pipeline is already loaded.

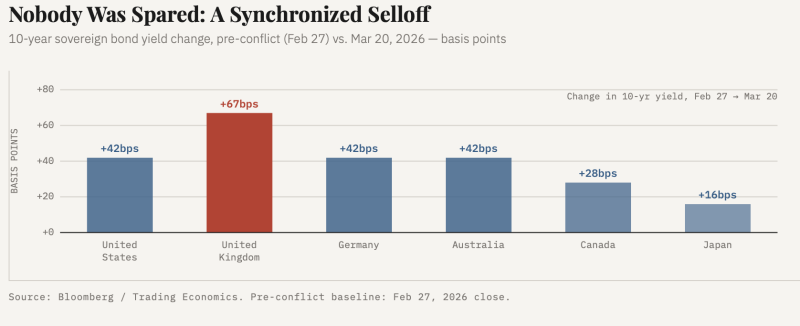

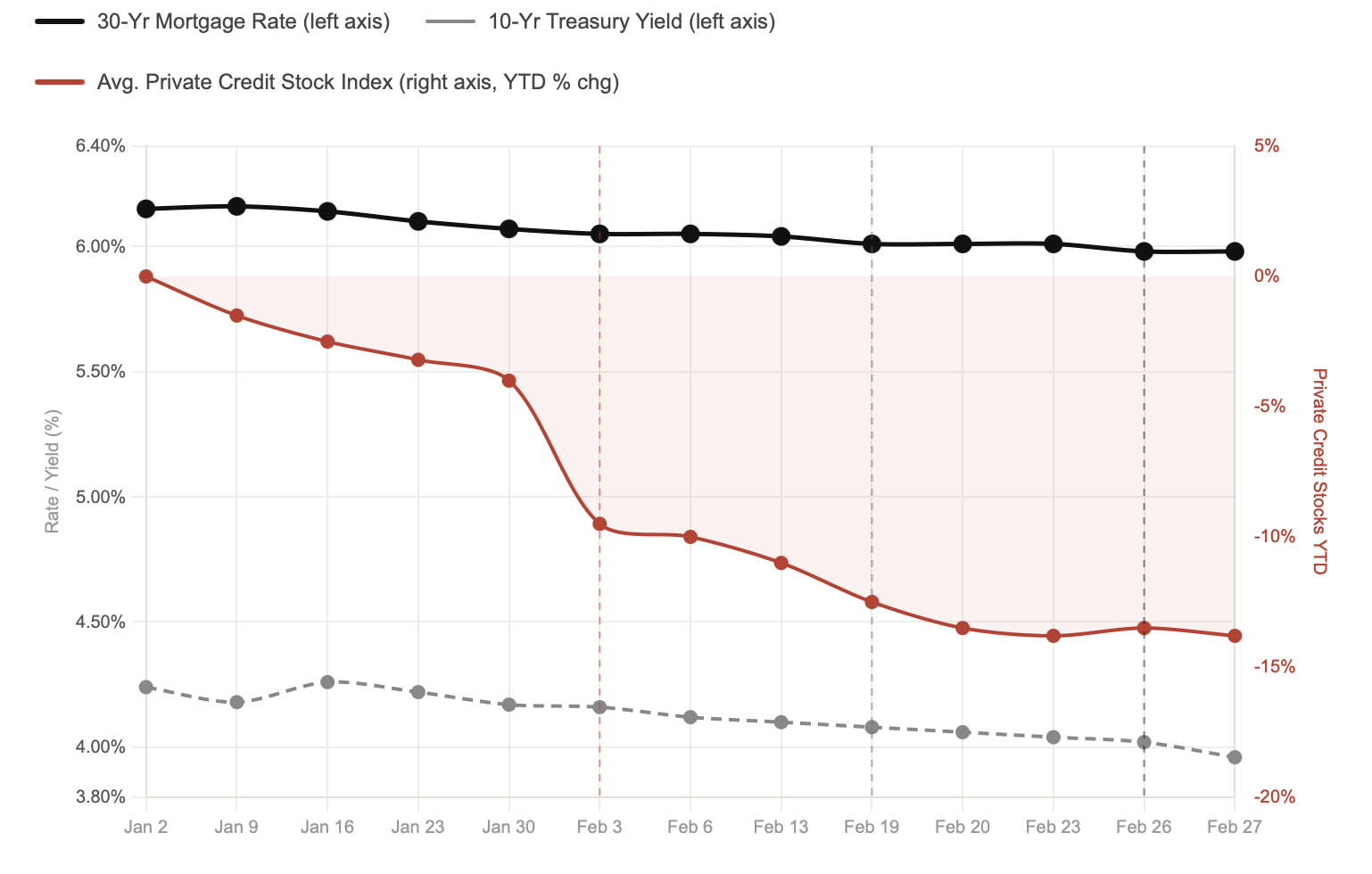

The World Reprices Risk

It would be one thing if rising Treasury yields were a purely domestic story, the Fed on hold, U.S. inflation stubborn, bond investors demanding more compensation. That is a familiar environment. What happened last week was different in character.

The 10-year Treasury yield added nearly 11 basis points on Friday to reach 4.39%, its highest level since July 2025, as the 30-year approached 5%. But that move did not happen in isolation. On the same day the Fed held in Washington, the Bank of England, the ECB, Sweden’s Riksbank, and the Swiss National Bank all held rates, each citing the war’s uncertain impact on inflation and growth. The Bank of England’s Monetary Policy Committee voted unanimously for the first time in four and a half years. Markets responded by pricing in a rate hike from the Bank of England as soon as this year, a complete reversal of the easing path that had been in place weeks earlier. The ECB revised its 2026 headline inflation forecast to 2.6%, up from 2.0% in December, driven almost entirely by energy, as traders began pricing in potential ECB rate hikes later this year as well.

When yields rise in one country, it reflects that country’s specific conditions. When they rise simultaneously across the U.S., UK, Europe, Japan, and Australia in the same week, driven by the same oil shock feeding into the same inflation expectations through the same transmission channel, it means the global rate-cutting cycle that the bond market spent 2025 positioning for has been interrupted at the source. That repricing does not stay contained to sovereign debt. It flows through to MBS spreads, to mortgage rates, and to the monthly payment on every home purchase contract being written right now.

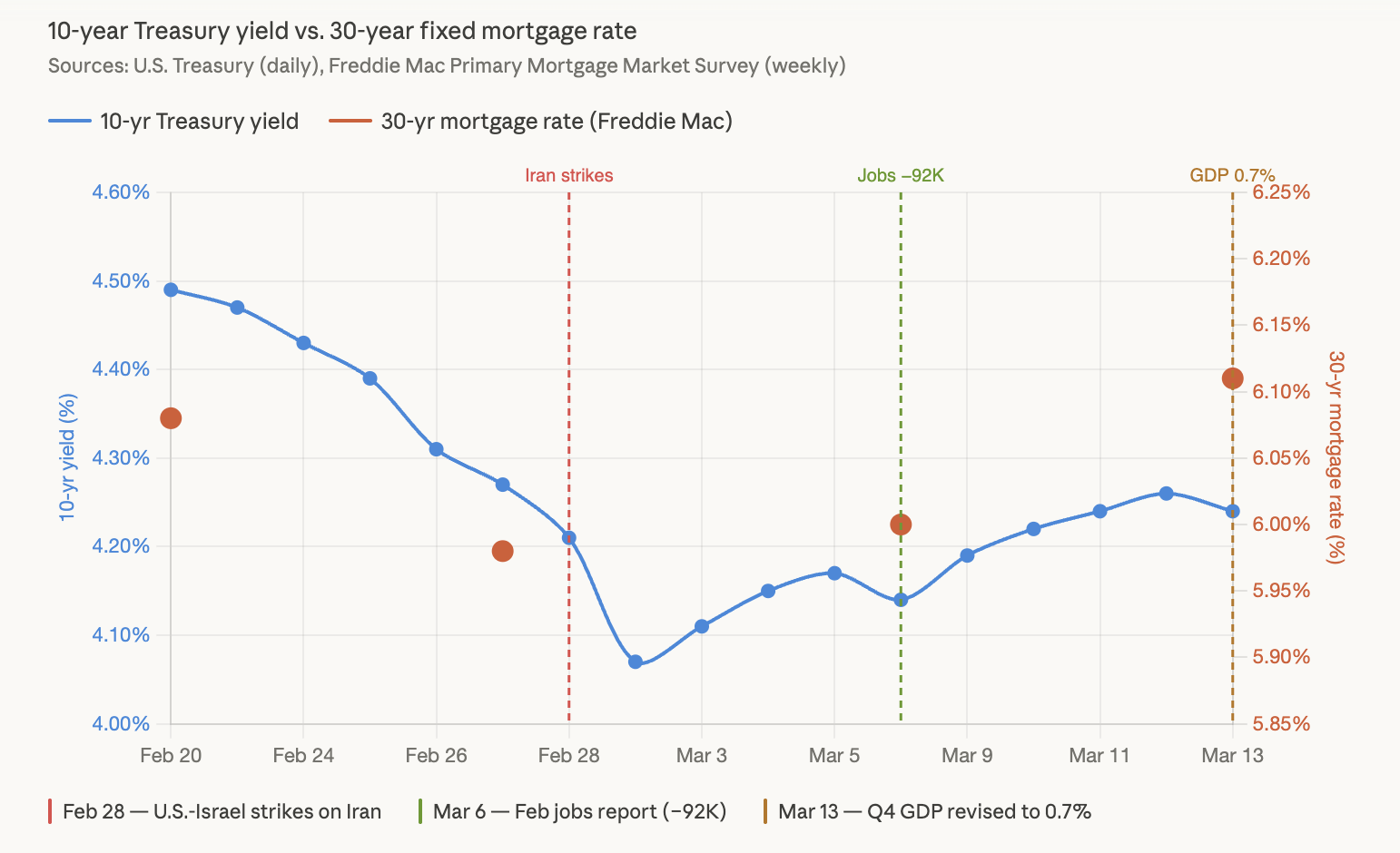

What It Means for Your Rate

The average 30-year fixed mortgage rate was 6.11% in the week ending March 12, according to Freddie Mac, the biggest weekly increase since Liberation Day tariffs caused bond yields to spike in April 2025. As of this writing, rates are trading closer to 6.2% and analysts covering the housing market are openly discussing a range of 6.5% to 6.75% if the 10-year yield holds above 4.4% through the spring.

The conflict has pushed MBS spreads to their widest levels since December 2025, more than fully offsetting the tightening that had occurred in January. That spread widening matters independently of where Treasuries are. Even in a scenario where the 10-year yield stabilizes, wider MBS spreads mean mortgage rates stay elevated relative to what the Treasury market alone would imply.

The underlying demand is real. Inventory has improved relative to 2024. Affordability, measured against where rates were a year ago, is modestly better. But the rate environment that was supposed to unlock that demand has closed, and what replaces it depends entirely on a military and diplomatic situation that no mortgage desk can model.

Leave a Reply