- The 30-year fixed averaged 6.23% last week, 58 basis points below where it was a year ago and at its lowest level across the last three spring homebuying seasons.

- The April 28-29 FOMC meeting is a hold, but the real event is what surrounds it: Powell’s likely final press conference as chair, and a Kevin Warsh Senate Banking Committee confirmation vote expected the same day.

- Warsh’s path cleared Sunday after the DOJ dropped its investigation of Powell and Sen. Tillis lifted his blockade, but a new chair who shifts how the Fed communicates could introduce spread volatility before his first meeting gavel falls.

- FHFA launched VantageScore 4.0 at the GSEs this week, giving lenders a new tool to reduce pricing costs for borrowers under 720 FICO, with meaningful savings available for those who know how to use it.

The mortgage market is heading into one of the more consequential weeks of the year, and the rate decision is the least interesting thing on the calendar.

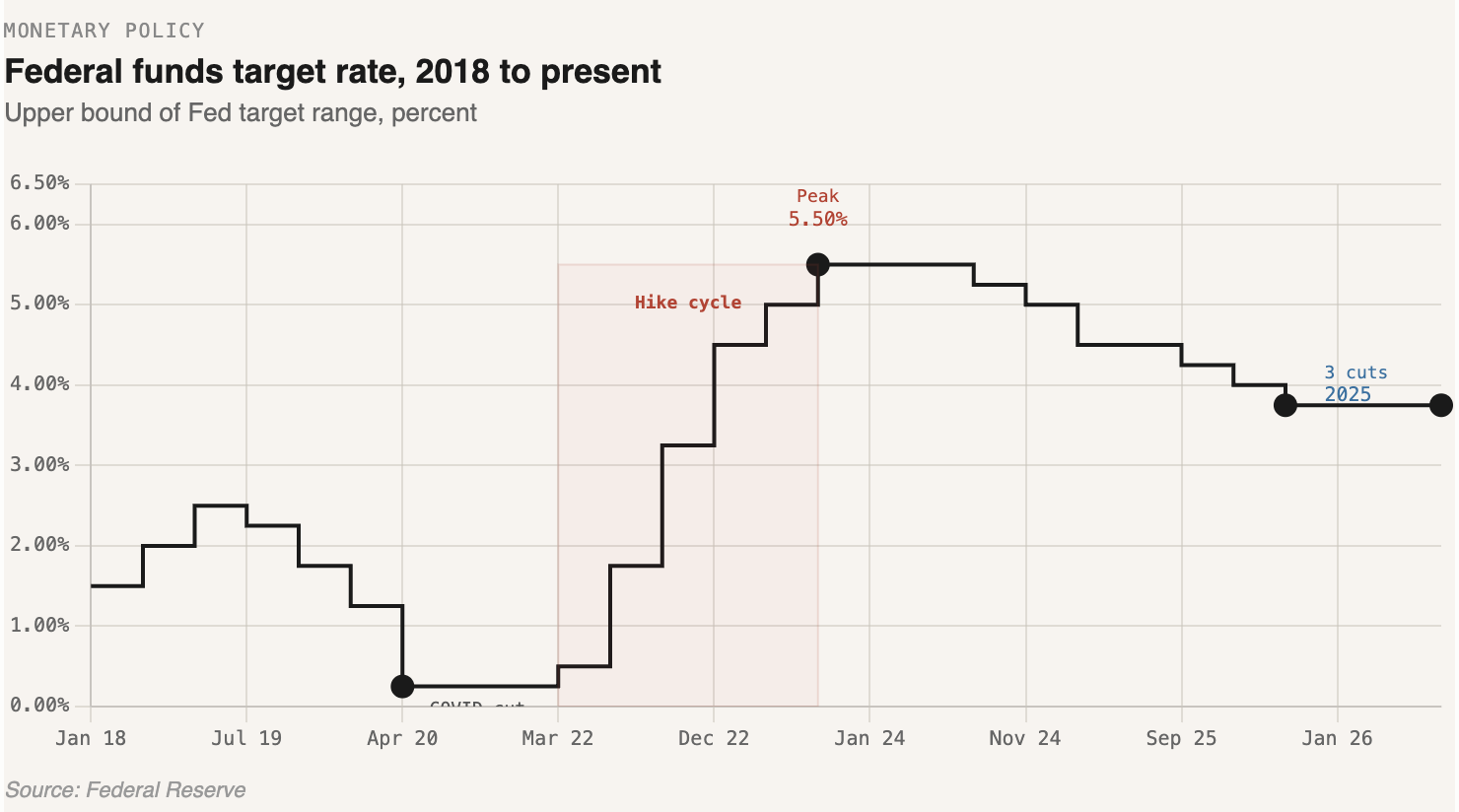

The FOMC meets Tuesday and Wednesday and will hold. The funds rate stays at 3.50% to 3.75%, where it has been since December 2025. That outcome has been priced in for weeks. What has not been fully priced in is what happens around it. Jerome Powell’s term as Fed chair expires on May 15. The April 28-29 meeting is almost certainly his last in the role. The Senate Banking Committee is expected to vote on Kevin Warsh’s confirmation on Wednesday, the same afternoon as Powell’s press conference. By the end of this week, the leadership of the most important financial institution in the world will have effectively changed hands, and the mortgage market will be left to figure out what that means for rates.

Where Rates Are

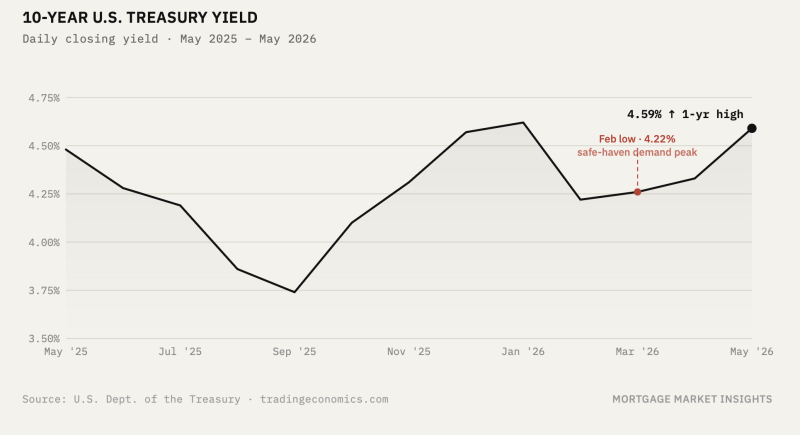

The rate picture entering this transition is about as favorable as it has been in three years. The 30-year fixed averaged 6.23% in the April 23 Freddie Mac survey, down 58 basis points from 6.81% a year ago. Purchase applications for the week ending April 17 were up 14.2% year-over-year. The spring market is responding.

The YTD path was not clean. The year opened with rates briefly touching under 6% in February as Treasury yields compressed on recession fears and safe-haven flows. March reversed that sharply. Firmer inflation data, rising oil prices from the Iran conflict, and a hawkish Fed sent the 10-year back up and mortgage rates followed, hitting a YTD high near 6.46% before April stabilized things. The full 2026 range has been 5.98% to 6.46%, a band that tells you exactly how unresolved the macro picture is.

On the MBS side, spreads have been range-bound for weeks. Current coupon OAS remain tight, and there is not much appetite among banks or money managers to push further at current levels. Mortgage REITs have been a constructive offset, growing their agency portfolios for nine consecutive quarters, but that demand has a ceiling too. The spread picture is stable, not improving, and how it evolves under a new Fed chair matters more than the current static read suggests.

Powell’s Exit

This week’s FOMC meeting is a non-SEP meeting. There is no dot plot, no Summary of Economic Projections, no updated rate path for markets to parse. What Powell gets instead is one final press conference and a statement that has to hold together under the weight of a genuinely difficult policy environment.

The March minutes were hawkish. Almost all participants supported holding. Some explicitly raised the possibility of rate hikes if inflation stays elevated. The dual mandate tension that has defined Powell’s final year remains unresolved: oil-driven inflation on one side, a softening labor market on the other. The statement language will not break new ground.

That discipline matters for mortgage rates more than it gets credit for. Powell’s consistent communication framework, press conferences after every meeting and deliberate forward guidance, helped keep MBS spread volatility contained even when Treasury yields were moving sharply. The market priced Fed intent with reasonable accuracy. You could argue that such reliability has a value that is easy to underestimate until it is gone.

Warsh has already signaled he intends to test it. At his confirmation hearing he was openly critical of forward guidance as a policy tool, arguing that the Fed speaks too frequently and that truth-seeking matters more than repetition. He declined to commit to post-meeting press conferences. For the mortgage market, that is not an abstract philosophical shift. Forward guidance is what allows originators, hedgers, and MBS investors to position ahead of Fed moves with some degree of confidence. Remove that anchor and the market has to reprice uncertainty in real time, which means wider spreads, more volatile pipelines, and a less predictable transmission from Treasury yields to mortgage rates. The question is not whether Warsh will cut. It is whether the market will be able to see it coming.

The New Fed

Warsh’s path to confirmation cleared after the DOJ dropped its criminal investigation of Powell, removing the one obstacle that had kept Sen. Tillis in opposition. The committee vote is Wednesday. With the Republican majority intact, full Senate confirmation follows shortly after and Warsh takes the chair by May 15.

His confirmation hearing last Tuesday offered a preview of the direction. He committed to independence, rejected the idea that he would cut rates on presidential command, and called for a new inflation framework and a more rules-based approach to policy. He also declined to commit to holding a press conference after every FOMC meeting, a meaningful signal. If Warsh reduces that cadence, the market loses a regular communication anchor and interpretation risk between meetings increases. That kind of uncertainty does not stay contained to Treasuries. It finds its way into MBS spreads.

The bigger question is timing. Markets are already pricing in a Warsh-led Fed as relatively more dovish than the current committee composition suggests. That pricing is part of why rates are at their best level in three spring seasons. But Warsh would need to build consensus on a committee where several members have recently flagged the possibility of hikes, and where energy-driven inflation gives the hawks a live argument. A new chair who moves too fast risks losing the committee. One who moves carefully may disappoint a market that has already leaned into the rate-cut narrative. Either outcome has direct implications for where mortgage rates go from here.

VantageScore: A New Pricing Tool for Lenders

This week FHFA announced that the GSEs would begin accepting VantageScore 4.0 immediately through a pilot program covering 21 lenders. That group represented roughly two-thirds of GSE issuance in the first quarter, meaning most borrowers working with a major lender will have access within weeks.

This is the change that matters operationally. The GSEs have used classic FICO exclusively to set loan-level price adjustments, the LLPAs that determine how much a borrower pays based on their credit score and loan-to-value ratio. VantageScore 4.0 scores the same borrower population using a different methodology, and it tends to rank lower-FICO borrowers relatively higher than classic FICO does. The GSEs are designing the VS4 LLPA grid to be revenue-neutral on average, meaning the same pool of borrowers generates roughly the same aggregate fees under either system. But the distribution of who pays more and who pays less shifts significantly.

The operational detail that matters for lenders: originators in the pilot can pull both a classic FICO and a VS4 score for the same borrower and submit whichever produces the better LLPA. The borrower does not see this process. The lender runs the comparison and delivers the score that reduces the fee.

For borrowers under 720 FICO, running that comparison is almost always worth it. Low-FICO borrowers are systematically ranked higher under VS4, and the LLPA savings are real. On a $350,000 loan, every point of LLPA is worth $3,500 in delivery fees. A borrower in the 640-659 FICO range could see savings of 25 to 50 basis points or more by switching to VS4, depending on LTV. For a borrower above 720 FICO, the math generally runs the other way. VS4 is unlikely to help and can produce a worse outcome. Those borrowers stay on classic FICO.

Two caveats worth tracking. FHA is not on the same timeline. HUD indicated it will take at least several months to bring VS4 online for FHA-insured loans, which means the Ginnie Mae market stays on classic FICO for now. The second caveat is for MBS investors. The ability to cherry-pick between two scoring systems means the historical FICO distribution in an agency pool no longer means what it used to. Prepayment and default models were calibrated on a population of borrowers with no ability to switch scoring systems. That consistency is gone, and existing low-FICO pools face some erosion of the call protection investors underwrote when they bought them.

Leave a Reply