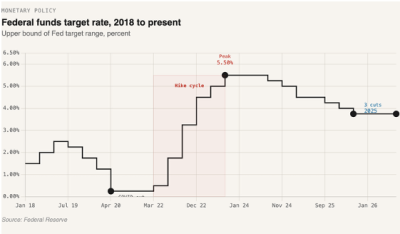

According to market pricing at the end of 2024, the Fed would have cut rates four times this year, with half of the cuts already in place by now. Since the last cut in December, the Fed Funds Rate hasn’t moved. After the first 50 bps cut in September 2024, mortgage rates have moved up within a 100 bps range. While this is very unusual, it’s not surprising. This is the bond market’s clear communication that the U.S. economy is not ready for a quick and large move down in benchmark rates.

Fast forward to today, and the sentiment hasn’t changed much. Yes, inflation has shown four consecutive prints of gradual cooling, and the same can be said for the labor market. But are things coming down at a pace that couldn’t reverse with easing? Most likely not, hence the extreme caution on the Fed’s side.

Most forecasts have revised their dot plot expectations for the year to one or no cuts. This is despite continuing jobless claims picking up and data pointing to a tighter job market for those who have lost their jobs. This suggests that the market is still waiting to see if the tariff impacts will show up in inflation, and to what extent. It seems the Fed is doing the same.

On the other hand, the administration wants to lower rates to avoid being stuck in the vicious cycle of issuing more and paying more to issue more. While the last 12+ months have been mostly calm in terms of Treasury issuance, the next 12 months are likely to be more exciting. At some point, the Treasury will have to announce that it needs to issue more debt, and the first thing the bond market will look at is how much the U.S. has been paying in interest. If the government kept spending at the same rate it was in Q1, then total annual interest payments would be over $1T.

The Fed, of course, is aware of this, but it also has a reputation to uphold, and that involves not flip-flopping with rates. It learned from the market’s reaction to the 50 bp cut that resulted in rates rising, i.e., term premia creeping back up. The Fed can control the benchmark rate, but it cannot control the term premia, so it will be very careful before the next move, despite being pressured to ease by 100 bps. The dot plots will continue to matter, but the same dot plots will continue to change as the facts (and sometimes, feelings) change.

Leave a Reply