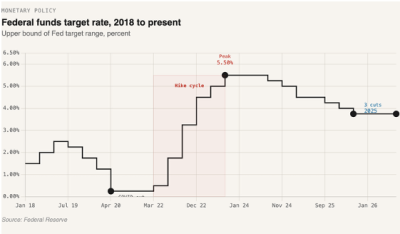

The 10YR has been drifting downward for nearly six weeks as markets begin to price in almost three rate cuts, with four Fed meetings remaining this year.

With bond yields falling and equities rising, markets are showing a fair amount of optimism, given where inflation and the labor market currently stand. We’ve seen this pattern before, and the cycle is likely to persist. The Fed has made no indication that it plans to move swiftly on rate cuts. While its dual mandate (price stability and maximum employment) gives no clear reason to cut, the unspoken “third mandate” is where the real pressure lies: the government’s interest expense.

Knowing that more government spending will be required in the coming years, the CBO is projecting deficits to get closer to 10% in the next two decades, indicating no slowdown of spending. A key driver is net interest that the US will have to finance by issuing as needed. The chart below illustrates this problem as the primary deficit (difference between revenue and spending excluding interest) is projected to be flat through 2046. It’s the net interest projections where the pain is.

The Fed knows this. But its job is to manage inflation and employment, not fiscal balance sheets. Still, the conundrum is clear: higher rates mean higher borrowing costs, which, in turn, can stoke inflation if the government continues to issue more debt at elevated rates. We’re just beginning to see signs of this feedback loop, which helps explain the growing chorus calling for lower rates.

But can Powell actually cut rates without sparking another inflation spike? If we focus on core inflation components, it’s clear we’re stuck for now. Headline inflation has been easing gradually, but services and housing continue to put a floor under price pressures, keeping the Fed’s 2% target out of reach.

The Fed is unlikely to deliver three cuts unless the services component of inflation eases up. The dot plot still shows two cuts for the year, but that could have been for the sake of stability. Next year’s path in the dot plot doesn’t give us much indication with Powell’s term ending in May. While the market is frontloading the cuts to this year and early next, the cuts are more likely to be delivered in the second half of next year. Until then, we are likely to see much of the same with small pockets of rate drops without any meaningful move in downward direction.

Leave a Reply