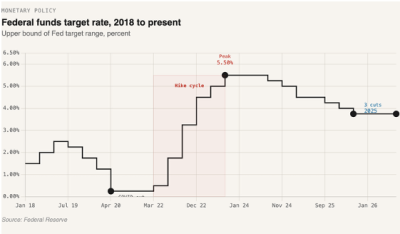

The much anticipated September Fed meeting will likely deliver a cut, probably a quarter point, even with pressure for more. While the drama around individual officials keeps attention on monetary policy, fiscal dominance has arrived quietly. It makes sense to lower benchmark rates when the government expects heavier bond issuance and more spending. Letting the fiscal side guide monetary decisions can create second order effects that are easy to miss.

The need for fiscal dominance has brought much criticism to the Fed, challenged Fed members’ employment status, including Powell’s, and turned the most hawkish members into doves. Change always matters, but what matters more is the rate of change. The rate of change at the Fed has been accelerated with resignations, mindset shifts when it comes to policy and regulation, and a new Fed framework. The Fed is changing, and it has to, in order for fiscal dominance to work.

A dovish Fed and additional policy cuts might suggest lower mortgage rates. The long end is not convinced and the two prominent mortgage forecasts agree. MBA and Fannie Mae both show the average mortgage rate through 2026 at or above 6.5 percent, driven by a 10YR yield that sits in the fours. Fed pressure moves the short end, which is where most government issuance lives. It does not do much for the long end because deficit spending can spur inflation and inflation tends to push long rates back up. That is the logic behind a bond market that is pricing more persistent inflation.

With rates not changing much the housing market will start seeing more markets with no or negative price appreciation, although the magnitude is unlikely to be crash worthy. This is reflected in the -0.2% home price growth in MBA’s forecast in 2026. While originations will see modest year-over-year growth, the peak opportunity for refinances has already materialized and will continue to be at about a third of total origination volume through 2026. This all goes to say that the Fed will change, the benchmark rate will change, more liquidity will be injected into the economy, but the mortgage market will remain very much the same.

The Fed may pivot. the mortgage market will not. Until treasury supply lightens or spreads narrow, rates will sit near current levels. Watch issuance, volatility, and the mortgage Treasury basis. That is the story that will decide the next leg.

Leave a Reply