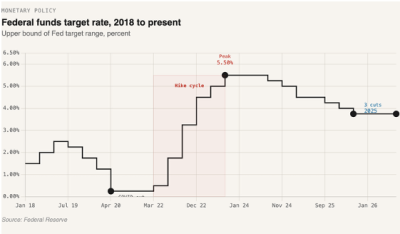

The part of monetary policy that often goes unnoticed until problems emerge is the Fed’s management of liquidity. This is a constant focus for the Fed, and over the years, it has refined its approach to avoid large market disruptions while tightening financial conditions. Managing liquidity is central to the Fed’s ability to tighten or loosen policy. We’ve been in tightening mode for more than three years, and this time, the Fed came prepared not to repeat the mistakes of the 2019 repo crisis.

To manage the flow of money, the Fed relies on two key facilities: the Reverse Repo and the Standing Repo. In periods of excess liquidity, the Fed uses the Reverse Repo to borrow cash overnight from banks using U.S. Treasuries as collateral. This process temporarily removes cash from the financial system, reducing the money banks can lend and helping to tighten conditions. The Standing Repo, introduced in 2021, does the opposite. It allows banks to borrow from the Fed at the upper bound of the Federal Funds Rate, providing a quick source of liquidity when needed to prevent short-term funding stress.

How do these facilities relate to mortgages? Both influence the overall cost of funding across the financial system, which in turn affects mortgage rates. Mortgage lenders rely on warehouse lines and other forms of short-term financing that are ultimately priced relative to broader market rates such as SOFR and Treasury yields. When the Fed adjusts the Reverse Repo rate, it alters the floor for these short-term rates and can indirectly push funding costs higher throughout the system. Even if temporary, an increase in short-term borrowing costs can create enough uncertainty to move mortgage rates higher until markets stabilize.

Earlier this month, the SOFR rate, the rate used for overnight borrowing between banks and the Fed, briefly exceeded the upper limit of the Federal Funds Rate.

At the same time, borrowing from the Standing Repo facility increased.

This behavior could suggest one of two things:

1. Liquidity is being drained from the system, signaling that the Fed may need to end QT immediately.

2. Banks are exploiting a pure arbitrage opportunity.

The first explanation is straightforward: banks are borrowing more and lending less, pushing overnight rates higher, even beyond the Fed’s target. That indicates stress in the system, suggesting the Fed might need to inject liquidity to stabilize rates.

The second scenario is more intriguing and reflects the nature of financial markets. When banks borrow from the Fed, the rate charged is the upper limit of the Federal Funds Rate, currently 4.25%. The SOFR rate, what the Fed pays when borrowing from banks in the Reverse Repo, is typically lower. However, when fewer funds are available for the Fed to borrow, SOFR rises. Banks notice this and take advantage of the spread. Borrowing from the Standing Repo at 4.25% and lending overnight at 4.30% becomes a risk-free arbitrage play for a quick return.

The arbitrage scenario is the better outcome for rates, as it carries no long-term impact on funding costs. If liquidity were the true issue, rising funding costs would force the Fed to end QT and possibly restart QE to restore liquidity. Even then, renewed easing wouldn’t significantly affect mortgage rates, since the Fed would likely buy short-term Treasuries rather than mortgage-backed securities.

Mortgage rates, therefore, appear set to remain elevated for years. The MBA projects rates in the mid-6s through 2028, even as refinance activity rises. That suggests origination volume will be driven more by buyers adjusting to the new rate environment than by rates falling to meet demand.

Leave a Reply