- 2025 was defined by adjustment to the new rate environment, with risk migrating from mortgages into other fixed income assets.

- Mortgage spreads narrowed materially, with the 30 year and 10 year spread compressing to around 200 basis points.

- Lower volatility revived mortgage bond demand, lifting USMBS returns and improving borrower rate economics, driving a 20 percent increase in activity.

- These trends support continued stability into 2026, reinforcing liquidity and a healthier origination market.

The theme that shaped 2025 for the housing market is all market players adjusting to the “new” mortgage rate environment. The last two years weren’t very different from one another in terms of economic drivers and monetary policy. What differentiated 2025 from 2024 was risk migration from mortgages to other fixed income assets.

This shift is evident in mortgage spreads, whether we are looking as option-adjusted spread (OAS), primary secondary spread, or the 10YR and 30YR fixed rate spread. The most mentioned spread is the 30YR/10YR, which has now come down to 200 basis points, a significant improvement from above 300 basis points at its more recent peak.

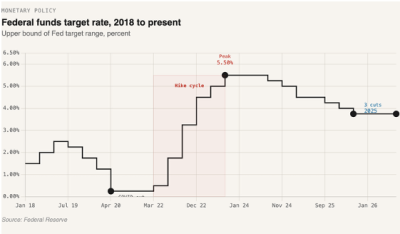

While spreads narrowing is a positive development for mortgage rates and costs, how this is happening is even more important. In markets risk never fades away or disappears. It simply migrates from one thing to another. Since the Fed began QT in 2022, a lot of risk got stacked on to mortgage rates, making spreads the widest they’ve been going back to at least early 2000s. Other fixed income assets, like US Treasuries didn’t see as much spread added to yields because inflation was so high and how the US was issuing debt helped keep yields normalized. So, mortgage spreads were wide at the expense of yield curve control and too much risk priced into mortgage rates, pushing the average rate to its highest in two decades.

Fast forward to the second half of 2025, mortgage rates began to see unusual stability thanks to low volatility. The stability helped bring more mortgage bond buyers into the market, pushed excess USMBS returns to their highest since 2010, spurring more investment and ultimately helped bring the cost of rates lower. With par rates improving, more borrowers were able to lock in better rates at lower or no cost, spurring a pick-up in mortgage activity by 20% compared to 2024.

These themes are likely to carry on in 2026, helping keep stability in mortgage rates. Stable markets are key for rate improvement and liquidity in markets that drive homebuying in the primary market. While there are many wildcards to consider in 2026, after years of market turbulence and many “new norms” the markets have adjusted and adapted to our current environment, which will continue to shape a healthier origination machine with stronger and more competitive players.

Leave a Reply