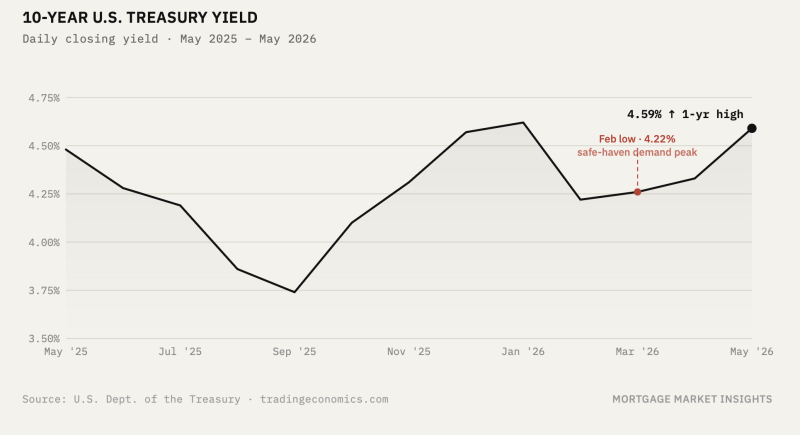

The bond market spent last week trading two completely different versions of the economy, sometimes within the same session. On Monday, the Strait of Hormuz remained blocked and oil prices reflected it. Futures markets responded by pricing out every rate cut on the calendar for 2026 and beginning to assign a small but nonzero probability to a hike next year. By Wednesday, the FOMC had held again, Powell had signaled he was not going anywhere yet, and the front end recovered some of what it had given up. By Friday, the market was still unresolved, waiting for something it could trade with conviction.

What Last Week Was Actually About

The Hormuz closure has now been the dominant variable in the Treasury market for weeks. What changed last week was not the situation in the strait, but what the market decided to do about it. That dynamic has continued into this week, with new proposals from Iran, new posturing from Washington, and oil prices moving on each development before any of it translates into an actual reopening. The back and forth remains to be the story.

Futures moved from pricing in modest easing late in the year to pricing in nothing, with a tail scenario emerging for a hike in 2027. That repricing was not driven by a data release. It was driven by the calculus that oil at current levels, sustained for long enough, feeds CPI, feeds PCE, and eventually forces the Fed’s hand even if the labor market is softening. The two scenarios are not compatible. The market spent the week toggling between them.

The dollar adds a layer to this story that tends to get skipped over in the rate narrative. The dollar has been weakening, sitting near two-year lows. A weaker dollar makes imports more expensive across the board. Historically a stronger dollar acts as a partial offset to inflationary shocks, absorbing some of the pressure before it reaches the consumer. That cushion is not there right now. The Fed is navigating an energy-driven inflation impulse without one of the tools that historically softens the blow, which tightens the bind further and makes the path back to 2% harder to model.

The Fed Meeting

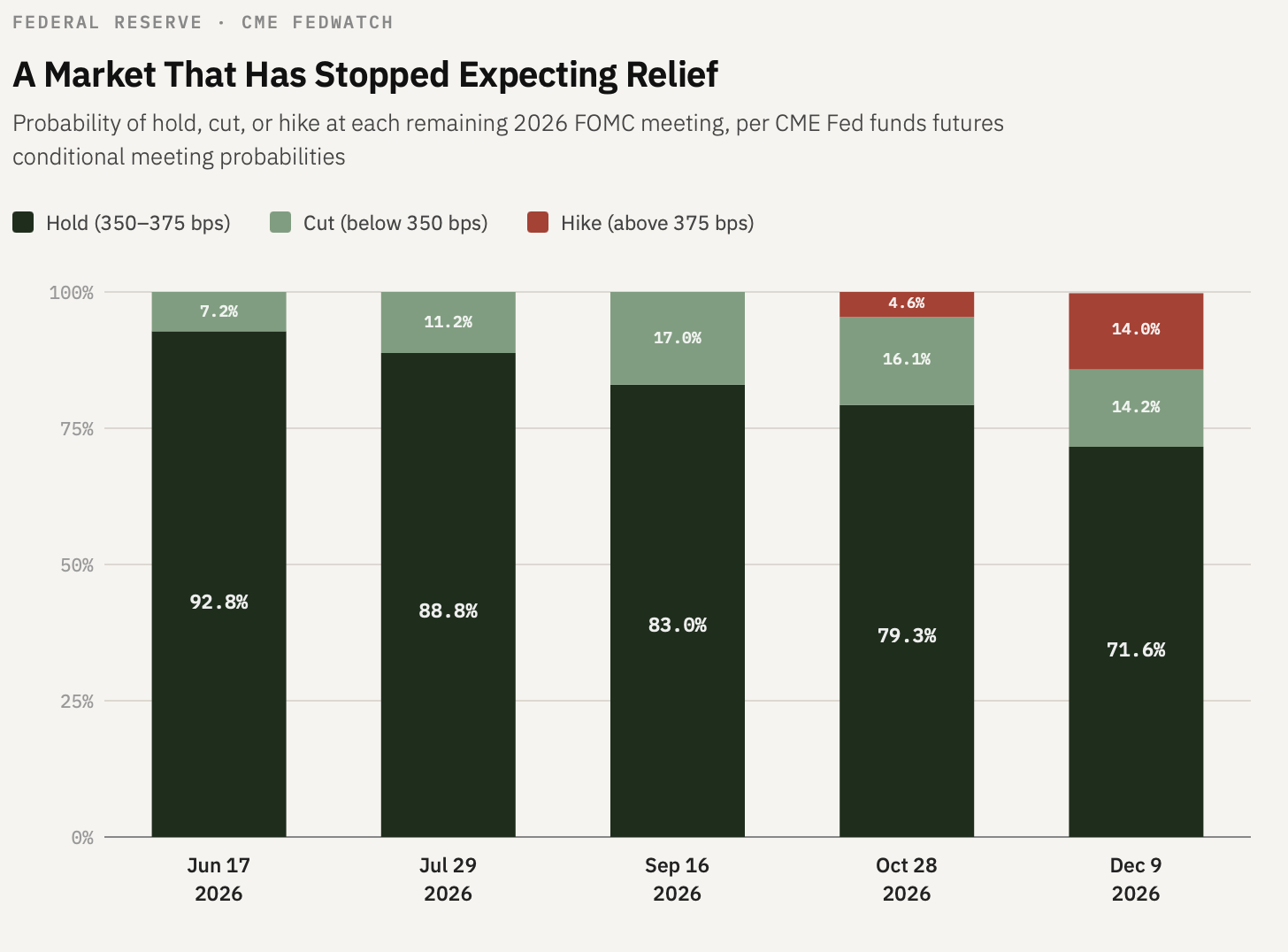

The FOMC held at 3.50% to 3.75%, as expected. What was not expected was the degree of division. The vote split 8-4, the most dissents at a single meeting since October 1992. The split was not clean. Three hawks opposed the easing bias embedded in the statement language, specifically the word “additional” in describing future rate adjustments, which implied the next move would be a cut. Miran, the dove, dissented in the other direction, preferring a cut at this meeting. A committee that is simultaneously too hawkish and too dovish to agree on a statement is not a committee that can offer the market a clear signal. That ambiguity is itself a rate input.

Powell announced that he intends to remain on the Board of Governors (for now) after his term as chair expires on May 15. Powell will remain a voting member through January 2028. On a committee already splitting 8-4, his vote does not become ceremonial because someone else is running the meeting. Warsh may run the meeting, but he does not run the committee.

Which brings the question of what a Warsh-led Fed actually looks like in practice. At his confirmation hearing he was openly critical of forward guidance as a policy tool, arguing the Fed communicates too frequently and that the signal has been diluted by repetition. He declined to commit to holding a press conference after every meeting. This matters directly to anyone pricing MBS or managing a pipeline. Forward guidance is what allows originators and hedgers to position ahead of Fed moves with some degree of confidence. Remove that anchor and the market has to reprice uncertainty in real time, which means wider spreads, more volatile rate locks, and a less predictable path from Treasury yields to mortgage rates.

It is worth remembering, though, that institutions have a way of moderating their critics. Scott Bessent came into the Treasury secretary role having been vocal about restructuring government debt issuance away from the bill-heavy approach Janet Yellen had put in place. The argument was straightforward: too much short-term financing created rollover risk and left the government exposed to rate volatility. Once in the seat, Bessent changed nothing of substance. The reason was equally straightforward: pushing more duration into the market would have put immediate upward pressure on long-term yields, with direct consequences for mortgage rates and the broader economy. The view from inside the institution looks different than the view from outside it. Warsh may find the same thing.

The Other Thing the Bond Market Is Watching

Wednesday’s quarterly refunding announcement from Treasury is not expected to deliver any surprises. The market is not positioned for one. But the debt picture remains a persistent undertow in the long end of the curve, and it is worth noting in the context of where mortgage rates go from here.

The decision to continue financing the deficit heavily through bill issuance rather than pushing duration into the long end has, intentionally or not, helped keep the 10-year and 30-year yields from moving as sharply as the inflation backdrop might otherwise suggest. A relatively anchored long end is a direct input into mortgage rates. That dynamic is running alongside the Fed’s continued runoff of MBS from its balance sheet, which removes a structural buyer from the agency market and puts ongoing upward pressure on spreads. The bill-heavy issuance strategy is partially offsetting that pressure by keeping duration supply contained. Neither force is going away, and how the government chooses to finance itself is not a neutral decision for anyone watching where mortgage rates settle.

Why the Jobs Report Is Conditional

This week’s employment data will be traded as a geopolitical event, not a labor market event. That sounds like an overstatement, except it is not.

Under normal conditions, a strong payrolls print pushes yields higher because it reduces the urgency for cuts. A weak print pulls yields lower because it reopens the easing path. Both of those reactions assume the dominant variable in Treasury pricing is domestic economic activity and the Fed’s response function to it. That assumption is not operative right now. The dominant variable is whether a barrel of oil stays elevated long enough to show up in the next two PCE readings, which then tells the Fed whether its next move is a cut or something else entirely.

A strong jobs number this week does not resolve that question. It adds pressure on one side of it, but if Hormuz remains effectively closed, the inflationary overhang does not go away because the labor market is resilient. A weak number is even more complicated. Softening employment would normally be a clear signal that the economy needs relief and cuts are coming. But a Fed facing simultaneous labor weakness and energy-driven inflation has no clean move. The jobs report will not break that bind. What it will do is give each side of the internal Fed debate more or less ammunition, without changing the fundamental constraint.

What Would Change This

There are three things that would restore data to its normal function in the rate market. A Hormuz resolution that credibly removes the oil supply disruption from the inflation outlook. An oil price decline sustained enough to change PCE trajectory. Or a labor market number so extreme in either direction that it overwhelms the geopolitical noise entirely. Short of one of those, this week’s jobs report will be interpreted through the same conditional lens that has defined every data release since the strait closed.

Until then, the market is not ignoring data. It is weighting it correctly, given what it knows. The problem is that what it knows is changing by the day, and the variable that matters most is not in any economic release.

Leave a Reply