Higher for longer has a new meaning. This phrase has served as a description of Fed policy. In the last month, the bond market reclaimed it as a verdict on the entire rate environment, one that has direct consequences for mortgage rates, servicing valuations, and the lenders caught between the two.

No Hope in the Bond Market

The bond market had been positioned, at least partially, for a diplomatic development that would take pressure off oil prices and, by extension, inflation expectations. When that development failed to arrive, the repricing was not a response to new information so much as the removal of a hope. Yields moved not because the data got worse but because the escape hatch closed.

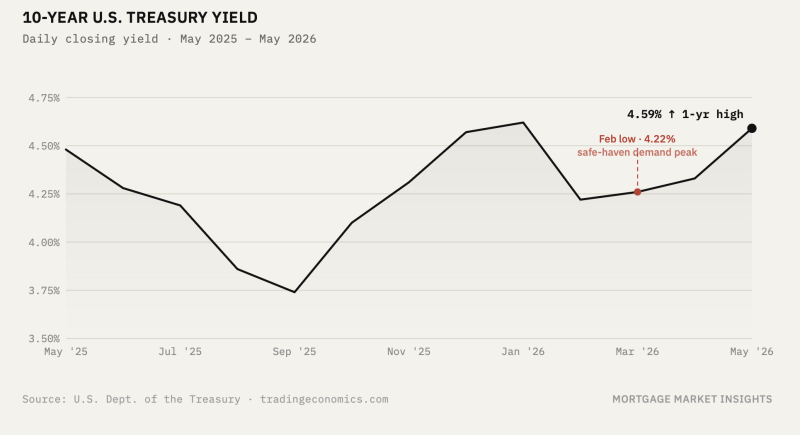

The 10-year Treasury yield climbed above 4.5%, reaching its highest level in a year. The move did not follow a single catalyst the way typical rate selloffs do. There was no surprise jobs number, no Fed pivot, no shock FOMC statement. The market has been waiting for a resolution from President Trump’s summit with Chinese leadership that might signal a path toward progress with the Strait of Hormuz. This has not materialized. The summit ended without any major agreements, including any indication that Beijing would help resolve the conflict. This follows both the CPI and PPI reports confirming that the energy shock is pushing inflation higher.

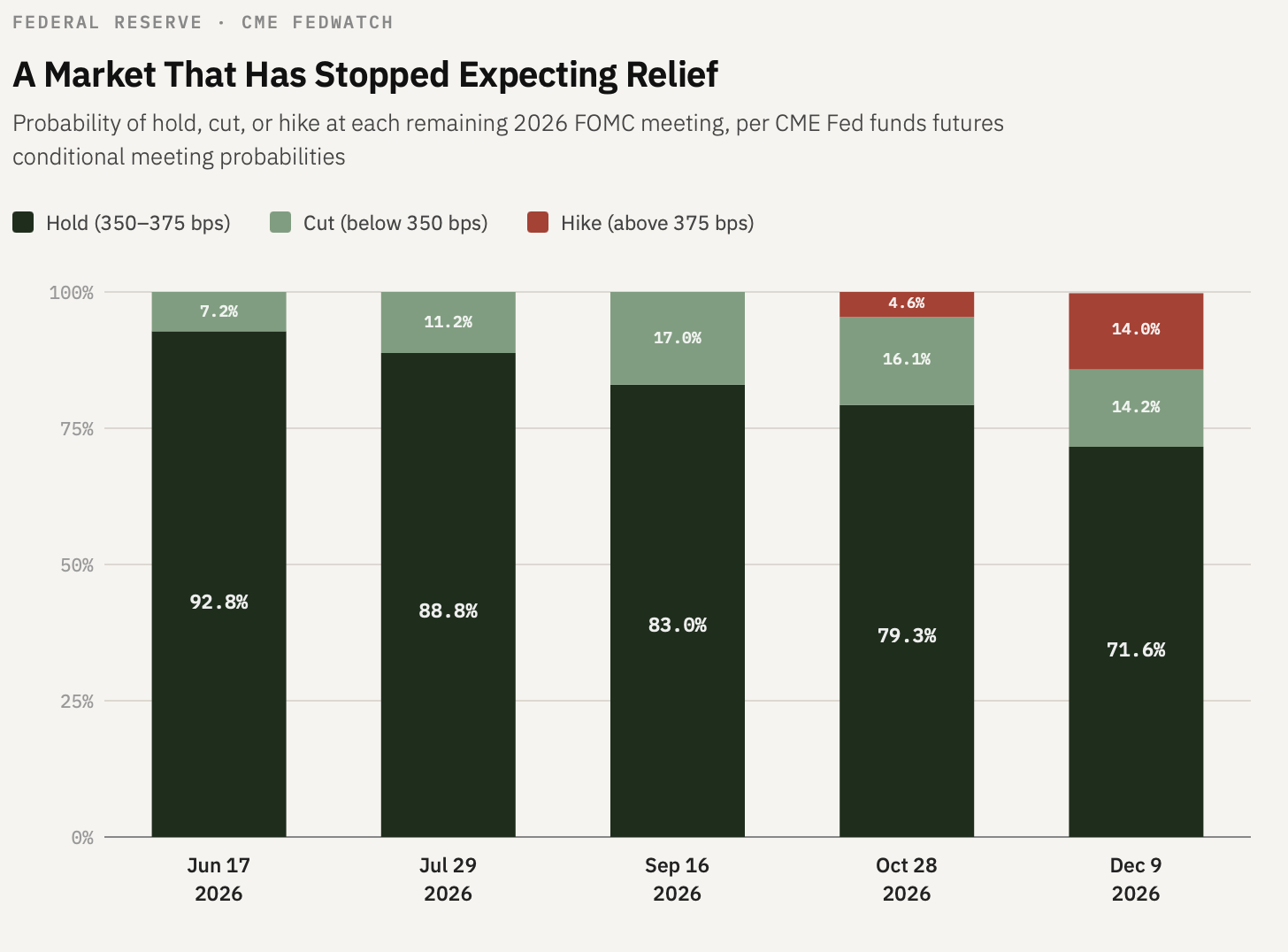

Traders are now pricing near-certainty that the Fed holds at its June meeting, with nearly 50% odds of a rate hike by year-end. That is a meaningful shift. Six months ago the question was how many cuts were coming. The question now remains whether the next move is up.

What the Data Confirmed

Consumer prices rose 3.8% year-over-year in April, the highest reading since May 2023, with energy accounting for more than 40% of the headline gain. The gasoline index is now up 28.4% annually. The Fed watches core inflation because it is supposed to capture durable price pressure rather than commodity volatility. Core CPI came in at 2.8% year-over-year, its highest monthly pace since January 2025. That is not a crisis number, but it is moving in the wrong direction, and it is doing so even before the secondary effects of an energy shock work their way through the supply chain.

Energy prices do not stay in the energy bucket. On the producer side, PPI rose 6% annually in April, the largest gain since December 2022, with the energy component up 7.8% for final demand goods. But the transmission into services was already visible: the services PPI accelerated 1.2%, its biggest monthly gain since March 2022, with two-thirds of that move attributed to trade services, a sign that tariff costs may be starting to spread more broadly through the pricing system.

The Fed’s mandate keeps its focus on core. But core is measured with a lag. Higher transportation costs feed into goods prices over several months. Fertilizer prices driven by energy costs move into food indexes. When producers face higher input costs, the pass-through to consumers is not instantaneous, but it is not optional either.

For mortgage rates, the implication is direct. The 30-year fixed sits at ~6.5%. That is nearly 50 basis points above where it briefly touched in February, when safe-haven flows into Treasuries compressed yields and produced sub-6% rates. Those flows have reversed. The bond market is no longer buying Treasuries out of fear; it is selling them out of conviction that inflation is not going away and that the next Fed move may not be a cut.

The Servicing Repricing

Mortgage servicing rights are valued on two primary variables: the value of future cash flows and the prepayment speed assumed for the underlying loan portfolio. When rates are elevated and refinance incentive is low, MSRs are generally more valuable because loans stay on the books longer, generating the servicing fee for an extended period. That logic held for most of the past two years and made servicing portfolios a reliable offset to compressed gain-on-sale margins.

The recalibration happening now is subtler than a simple rate move. Spec pool payups, the premium investors pay in the TBA market for collateral with better prepayment profiles, had climbed steadily as originators competed to deliver high-quality pools. Those payups reflected a market that had priced in a relatively stable rate outlook. That outlook no longer exists.

A market pricing in a potential hike next year has introduced a new tail scenario into prepayment models: one where rates move higher from here and extend loan lives further, but also one where any eventual geopolitical resolution triggers a refinance wave the models did not anticipate. Rate volatility compresses the value of optionality-sensitive assets, and MSRs are nothing but optionality-sensitive. Wider outcome distributions mean higher model uncertainty, which means less reliable marks and more volatility in reported book values.

The margin picture that results from combining lower origination volume with MSR mark uncertainty is asymmetric across the lender landscape. Large servicers have the balance sheet capacity to hold through valuation volatility rather than being forced to sell at distressed marks. Smaller originators do not. They could get squeezed from both directions: thin production economics at current rates, and servicing assets that are harder to value with confidence. Releasing servicing into a market where buyers are also uncertain about model assumptions does not produce favorable bids. Retaining it requires capital and tolerance for mark-to-market swings that can overwhelm operating income. Neither option is clean, and the institutions with the least flexibility are the ones with the least ability to wait it out.

The Bigger Picture

This week crystallized something that has been building since the Iran conflict began in late February. The rate environment is no longer driven primarily by domestic monetary policy. It is being driven by an energy shock with a geopolitical origin, transmitting through inflation data the Fed cannot easily dismiss, into a bond market that has repriced its expectations for the next two years of policy. Mortgage rates are downstream of all of it.

Higher for longer used to mean the Fed would not rush to cut. It now means the market is no longer certain the next move is a cut at all. For servicers, that changes the math on every portfolio assumption they hold. For originators, it means volume recovery is not on the near-term horizon. And for borrowers, the sub-6% window that briefly opened in February is closed, for now, by forces that have nothing to do with borrower credit profile and almost everything to do with a chokepoint in the Persian Gulf.

Leave a Reply